The CFO survey, in cooperation with the Richmond Federal Reserve Bank and the Atlanta Fed, was published on September 24, 2025. The survey was conducted with the participation of CFOs from large and small companies in the third quarter of 2025.

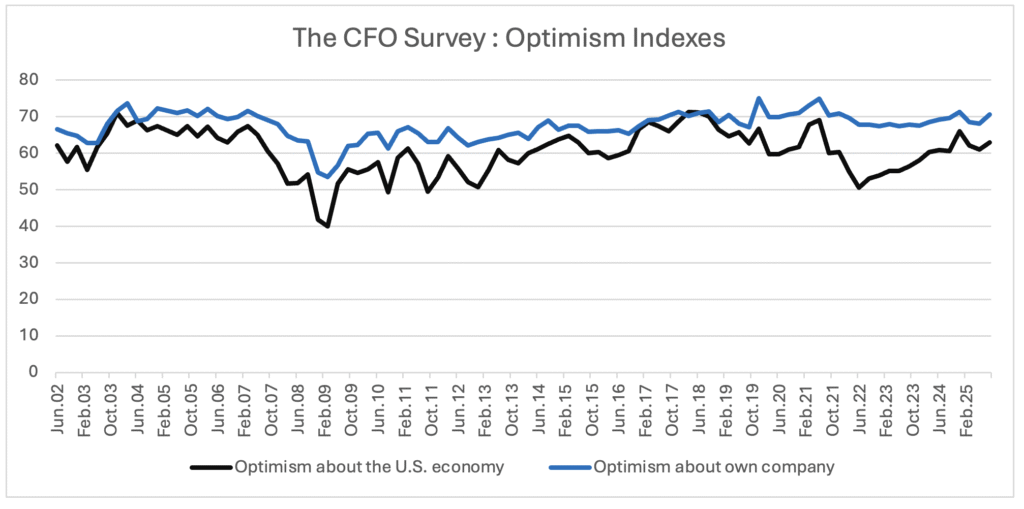

In this survey, conducted between August 18 and September 5, CFOs were asked to rate their optimism about the U.S. economy on a scale from 0 to 100. The average optimism percentage was 60.9% in the second quarter, while in this quarter it was calculated as 62.9%.

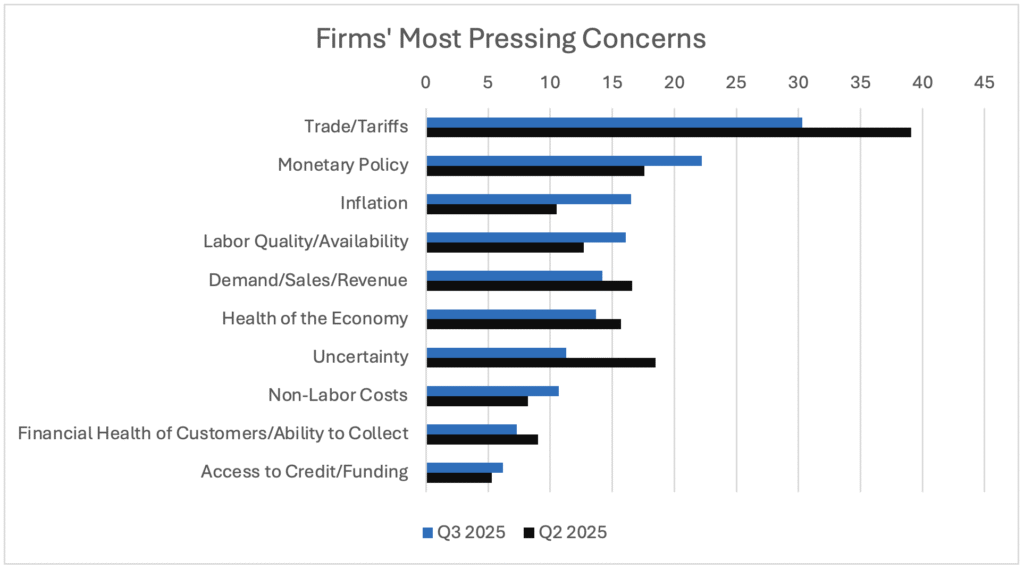

For the third consecutive quarter in 2025, CFOs’ biggest concern was trade policies and customs tariffs. Although it decreased compared to the second quarter, Trade/Customs Tariffs are still in the first place. Monetary Policy and Inflation followed in second and third place with increasing concerns, while concern about Uncertainty has declined.

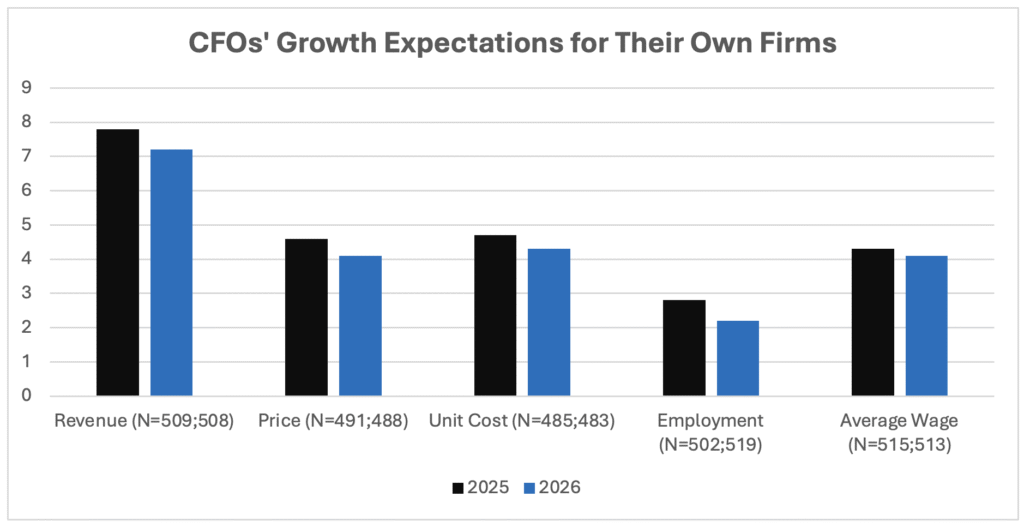

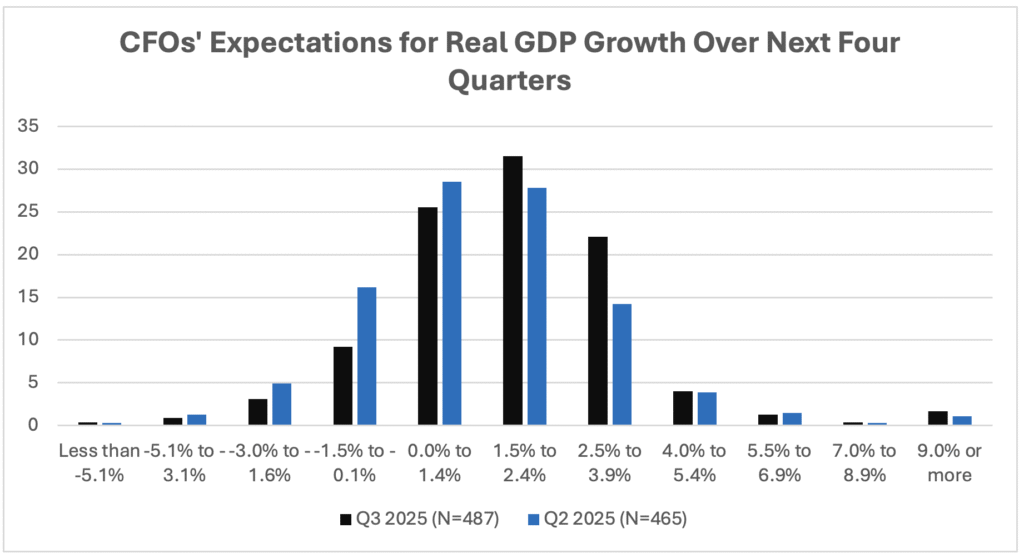

The growth rates expected by CFOs in the third quarter of 2025 are shown in the chart in below.

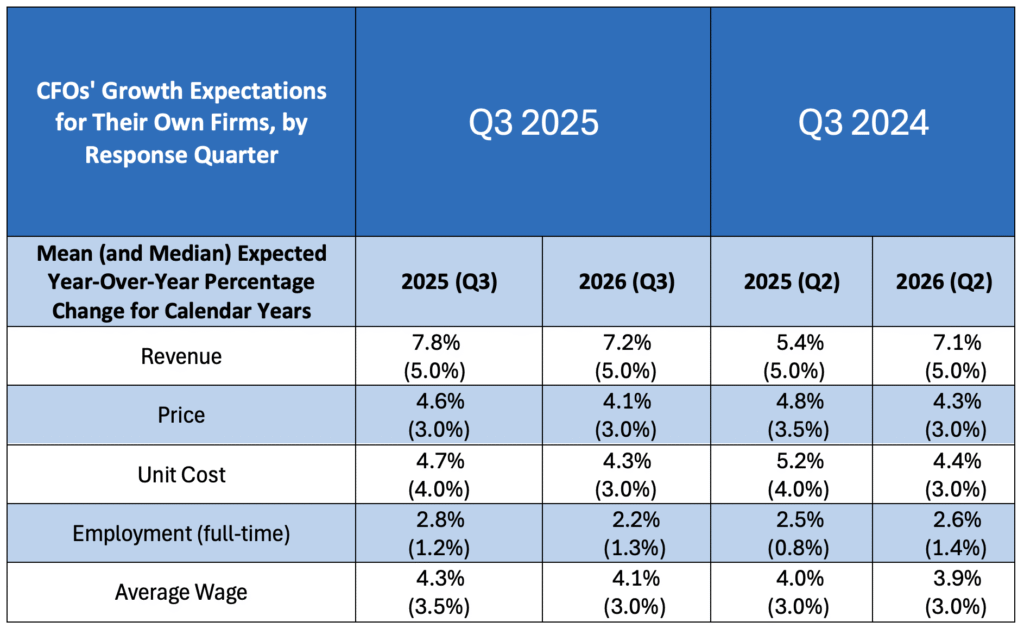

The growth amounts expected for their own companies in the third quarter are compared with the previous quarter in the table below. For 2025, the revenue growth expectation was 5.4% in Q2, while it increased to 7.8% in Q3. Employment growth expectations also rose from 2.5% to 2.8%, showing a limited but positive revision. On the other hand, the most significant decline was seen in unit costs; the expectation at 5.2% in Q2 decreased to 4.7% in Q3. Similarly, price increase expectations fell from 4.8% to 4.6%, presenting a more moderate outlook. For 2026, expectations generally remained stable, while a slight increase in revenue and a limited decrease in costs stand out. This table shows that CFOs are more optimistic about revenue growth in the medium term, while they have a more cautious expectation regarding cost pressures.

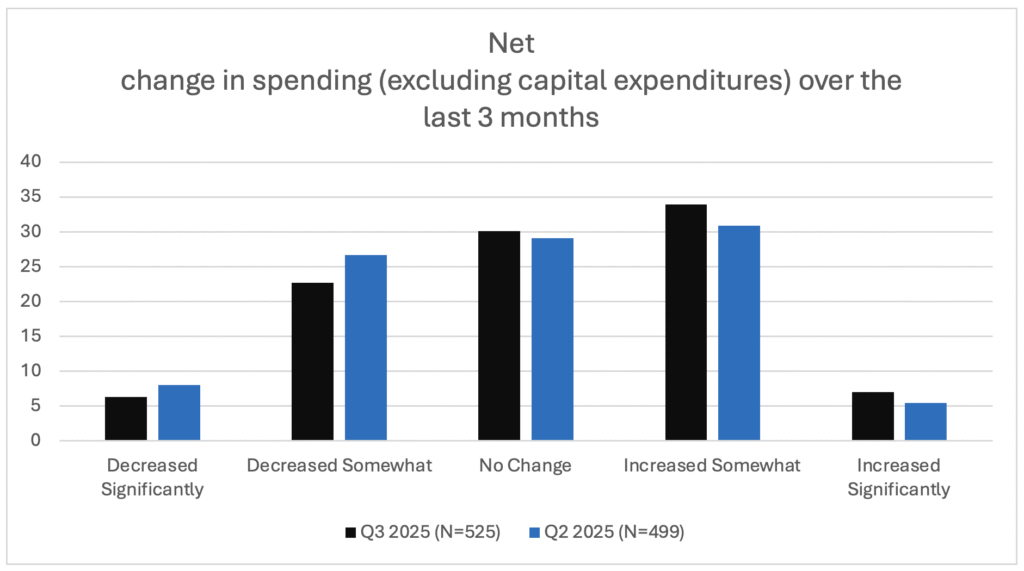

In the survey covering the past three months, the proportion of firms that increased their expenditures, excluding capital expenditures, rose from 36.3% in the previous quarter to 40.9%. This result reveals that companies displayed an upward trend in their operational expenses.

In the third quarter of 2025, expectations shifted markedly toward the middle ranges; the share of the 1.5%–2.4% band rose from 27.8% to 31.5%, while the share of the 2.5%–3.9% band increased from 14.2% to 22.1%. In addition, the probability of negative growth fell from 22.7% to 13.6%, confirming that perceptions of recession risk have weakened.

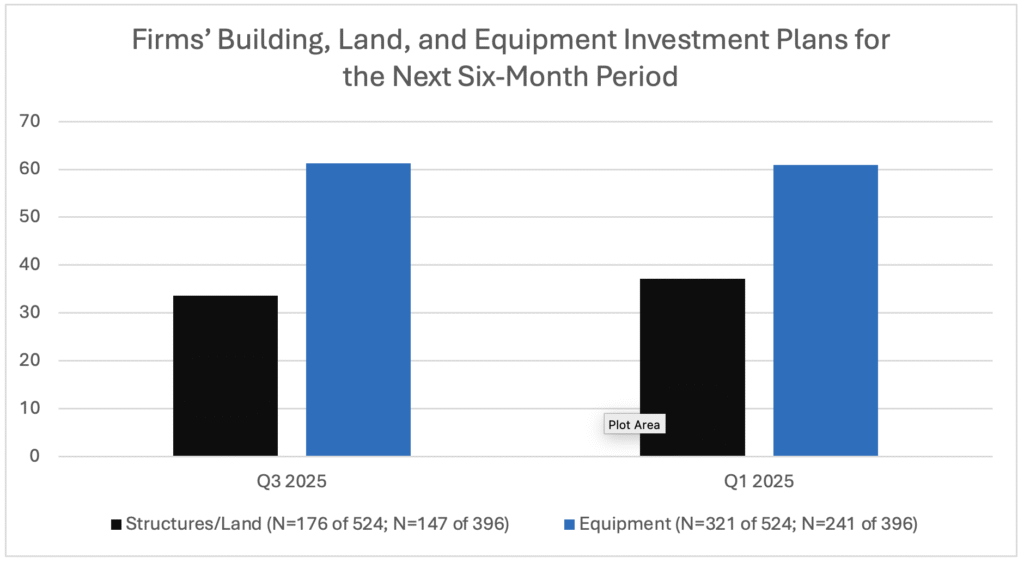

In the midyear investment module of the third quarter 2025 CFO Survey, companies’ investment plans for the next six months were addressed. According to the report, the proportion of firms planning building and land investments was 37.1% in the first quarter of the year, while it fell to 33.6% in the third quarter. In contrast, the rate of equipment investments has hardly changed; it was 60.9% in the first quarter and was recorded as 61.3% in the third quarter. These results show that companies follow a stable line particularly in equipment investments, while there has been a limited decline on the side of buildings and land.

The results of the third quarter 2025 CFO Survey show that repair and renovation stood out in companies’ investments. In buildings and land, this rate was 49.4%, while in equipment it was clearly the highest at 74.8%. Capacity expansion ranked second (38.6% and 46.4%), while new product and service investments remained more limited.

The most frequently stated reason by companies that did not invest was the lack of capacity need (58.3%). In addition, cash preservation (30.8%) and uncertainty (23.7%) were among the other prominent reasons. The lack of capacity need increased compared to the first quarter, while cash preservation and especially the uncertainty rate declined. This picture shows that companies are focused more on preserving their existing assets and maintaining stability rather than taking new growth steps.

The special questions of the third quarter 2025 CFO Survey present remarkable findings regarding companies’ investment, employment, and demand expectations. About half of the firms stated that uncertainties in tariffs and trade policies affect their price (46.5%) and cost (49.6%) expectations, while on the employment side, most companies plan replacement hiring (53.7%) or hiring for new positions (34.5%) during the rest of the year. On the other hand, 15% of the firms prefer not to fill open positions or to lay off workers, and the most prominent reasons behind this decision are demand uncertainty (56.9%) and financial constraints (54.2%). Demand expectations, however, are relatively optimistic: half of the companies (50.3%) expect demand to increase in the next 12 months, while one-third (32.4%) think current levels will be maintained. Overall, these results reveal that CFOs are taking cautious steps while considering risks, but they carry an optimistic expectation regarding demand growth in the upcoming period.

The results of the third quarter 2025 CFO Survey, conducted by the Richmond Federal Reserve Bank and the Atlanta Fed, reveal that companies maintain a cautious stance against risks while being optimistic about revenue growth and demand. Although trade policies and cost pressures continue to create concerns, a balanced approach stands out in employment and investment plans. This trend indicates that CFOs’ strategic decisions in the coming period will be shaped not by uncertainties but by expectations of sustainable growth.

References:

Richmond Fed. (2025, 24 September). CFOs Report Increased Optimism as Uncertainty Fades [Web sayfası]. Richmond Fed. https://www.richmondfed.org/research/national_economy/cfo_survey/data_and_results/2025/20250924_data_and_results