The latest CFO Survey, conducted by Duke University’s Fuqua School of Business in collaboration with the Federal Reserve Banks of Richmond and Atlanta, captures a dynamic pre- and post-election landscape. With insights from 515 participants, the findings underscore a mix of optimism about growth and caution around emerging challenges, especially on policies

Optimism and Economic Growth

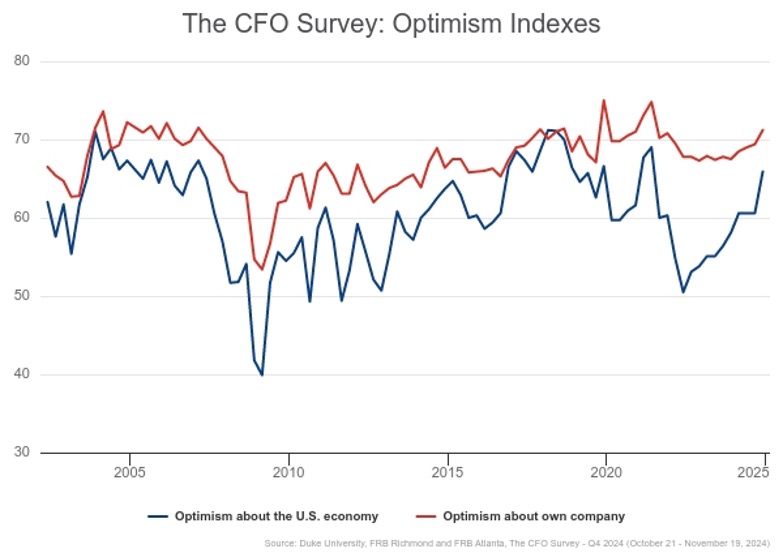

The survey conducted with 515 CFOs revealed a notable increase in optimism compared to the previous quarter, driven by clarity following the election results. CFO confidence in their own companies rose by approximately two points, from 69.4 to 71.2, while their outlook on the broader U.S. economy saw an even more substantial increase of nearly five points. This surge suggests that reduced political uncertainty may be positively influencing both corporate and economic outlook for growth. CFOs’ expectations for real GDP growth over the next four quarters saw a modest increase compared to the prior survey, reflecting a cautiously optimistic outlook on the broader economic trajectory.

Change Of Concerns with the New Policies

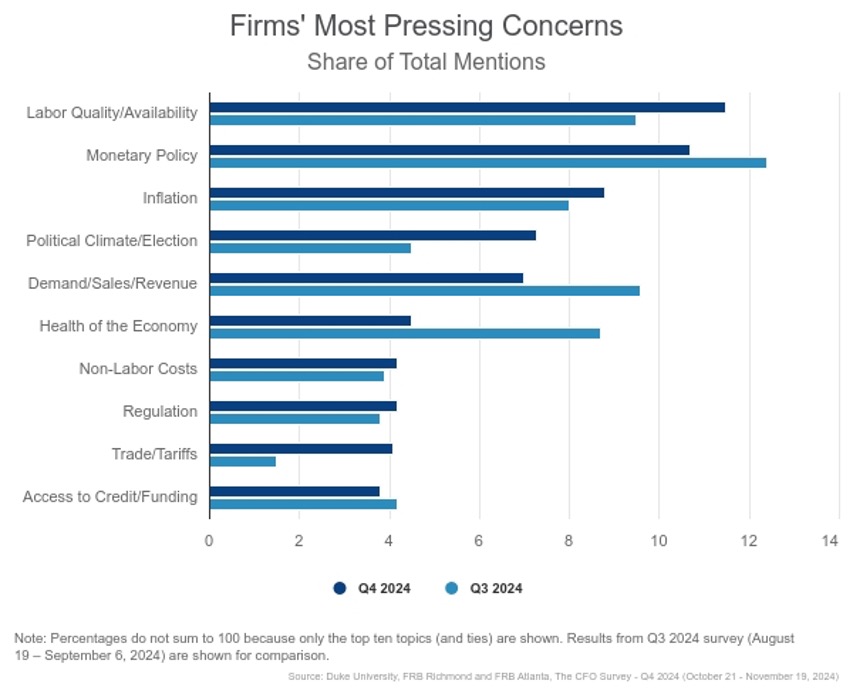

Before the elections, the labor market dominated CFO concerns, with the hiring and retaining the labor being the primary focus. However, following the elections, monetary policy took precedence, pushing labor availibity and quality worries into a secondary position. Inflation and the political climate also remained key concerns for CFOs, while tariffs, previously absent from the top ten issues, surged in importance, reflecting the evolving post-election priorities.

Expectations of CFOs in the Next Chapter

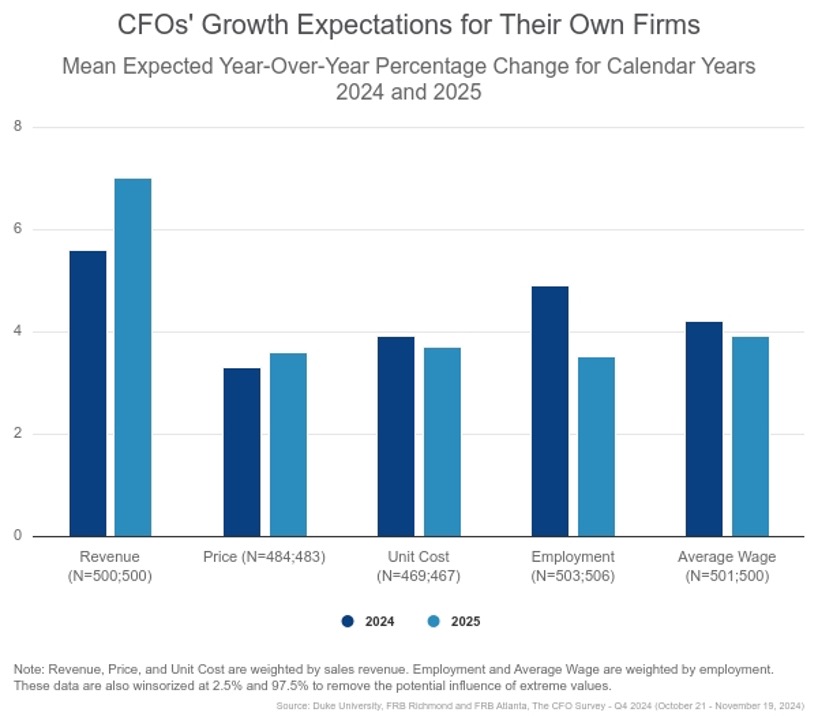

The fourth-quarter CFO Survey reveals a mixed outlook for 2024, with revenue expectations showing an increase while projections for price growth, unit costs, employment, and average wages all declined. This shift suggests cautious optimism about topline growth, tempered by more conservative expectations for operational and labor-related expenses. The share of firms reporting increased spending, excluding capital expenditures, declined to 41% in the past three months, down from 44.6% in the previous quarter. This decrease reflects a slight pullback in discretionary spending, potentially signaling a more cautious approach to managing operational budgets.

Relevancy of Policy Topics for CFOs

Pre-election responses, gathered from 252 participants, emphasized monetary policy as the most important issue, followed by U.S. corporate tax and regulatory policies. However, in the post-election survey, regulatory policies emerged as the top concern, overtaking corporate tax and monetary policy. This shift highlights the growing significance of regulatory matters, while corporate tax and monetary policies remain key considerations for CFOs.

Conclusion

The survey results reveal an economic outlook characterized by optimism for overall economy and concerns about policy changes. While confidence in growth remains strong, shifts in policy priorities and restrained spending indicate an environment where challenges persist. With the clarification of election results and indication of new policies, CFOs seem to be aware of changing atmosphere.